Stablecoins Disrupting Global Remittance: Inside KB Financial's PoC on Cross-Border Payments

Key Takeaways

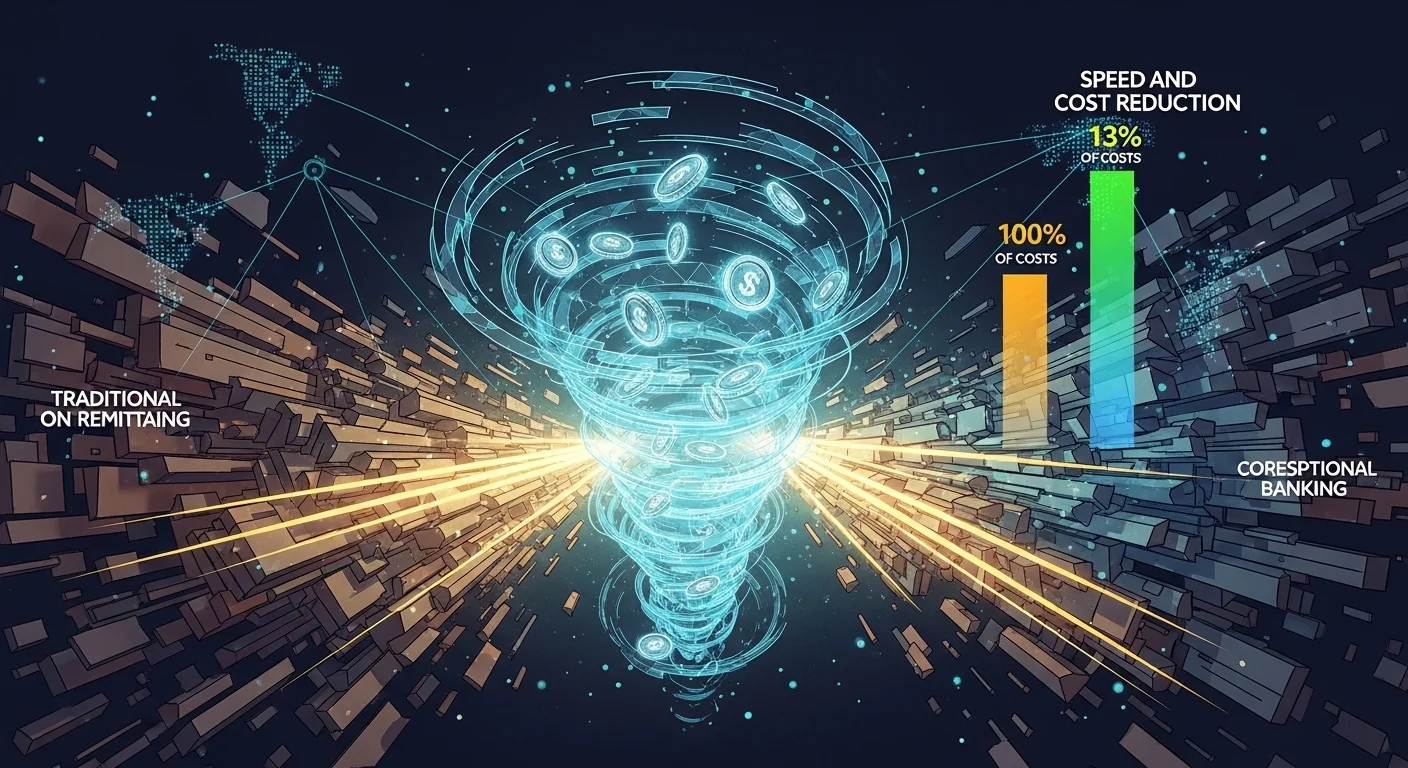

KB Financial's successful stablecoin pilot demonstrated that digital assets can slash remittance costs by 87% and execute international transfers in under three minutes, radically disrupting traditional correspondent banking.

The successful completion of a proof-of-concept (PoC) pilot by KB Financial Group represents a seismic shift in how global capital moves. By deploying a Korean won-denominated stablecoin for cross-border payments, the institution has demonstrated the technical viability and profound economic superiority of digital assets over traditional banking rails. This pilot did more than just test technology; it quantified the systemic friction inherent in legacy systems, proving that digital currencies can fundamentally rebuild the global remittance infrastructure, making international fund transfers faster, cheaper, and dramatically more efficient.

The modern cross-border payments landscape has long been defined by correspondent banking networks, most notably the SWIFT system. While robust, these mechanisms are characterized by high transaction costs, multi-day settlement times, and complex intermediary bank dependencies—a friction that disproportionately impacts migrant workers and small businesses reliant on timely payments. Stablecoins offer a potent technological countermeasure. They introduce a programmable, regulated layer of speed and transparency, utilizing blockchain technology to bypass the inherent inefficiencies of the global fiat chain. The core insight demonstrated by KB Financial is the ability to build a seamless, multi-currency bridge, transforming the stablecoin from a theoretical asset into a genuine, commercial utility for global commerce.

How Exactly Does Stablecoin Technology Solve Cross-Border Payments?

The technical elegance of the KB Financial PoC lies in its sophisticated ability to bridge the digital asset world with the established fiat banking infrastructure—a critical achievement for institutional adoption. The process flow mapped out for international remittances is a masterclass in interconnected financial technology.

Instead of relying on multiple layers of correspondent banks, the system initiates with the domestic won stablecoin. To reach a beneficiary in a different jurisdiction, such as Vietnam, the system utilizes the integrated on-chain liquidity mechanisms of the Kaia platform to execute a synthetic, multi-step conversion—from KRW-denominated stablecoin to USD-denominated stablecoin. This digital asset conversion is near-instantaneous. Crucially, the process does not end in the decentralized realm. The resulting dollar stablecoin is then channeled through a local banking partner to settle directly into the beneficiary's actual bank account. This controlled "on-ramp" from the blockchain to the local fiat system is the linchpin of the model, ensuring that while the rails are digital, the final settlement is universally accepted. The reported transfer time of less than three minutes fundamentally dismantles the concept of slow, batch-processed international finance.

The Economics of Speed: Analyzing Cost Reduction and Efficiency Gains

The most striking metric presented by the pilot is the dramatic reduction in transaction costs. The comparison to traditional methods, which often involve intricate correspondent bank fees and various overheads, revealed a staggering decrease in remittance fees—reportedly by approximately 87%. For the end-user, this cost efficiency translates directly into higher take-home pay for migrant workers and drastically lower operational expenditure for small merchants, stimulating grassroots economic activity in recipient nations.

Furthermore, the scope of the PoC suggests implications far beyond mere remittances. The ability to use a won stablecoin and link it to offline merchant payments indicates a path toward a fully digitized domestic payment ecosystem. This suggests that digital assets are not just an international tool, but a foundational layer for optimizing domestic liquidity, potentially accelerating the transition to a highly programmable domestic payment layer that integrates seamlessly with physical commerce. The focus on a comprehensive, internally designed process by KB Financial underscores a deep level of institutional commitment, treating the stablecoin not as a novelty, but as a core operational utility.

Key Facts

- Fee Reduction: Stablecoin utilization reduced remittance costs by approximately 87% compared to traditional SWIFT-based methods.

- Settlement Speed: The end-to-end international transfer was completed in under three minutes, a dramatic leap from multi-day legacy systems.

- Platform: The pilot was executed on the Kaia platform, demonstrating global layer-1 interoperability and liquidity integration.

- Technical Leap: The system successfully bridged digital asset rails (stablecoins) with traditional banking rails, enabling seamless settlement.

The Future of Finance: Implications for the Global Economy

The success of this pilot highlights a critical trend: the merging of decentralized finance (DeFi) efficiency with established financial infrastructure. For the global economy, this means enhanced efficiency, reduced counterparty risk, and a democratization of cross-border capital movement.

Regulatory Considerations: The ability to process high-value, low-friction payments at speed is transformative. However, the success of the rollout hinges on regulatory clarity. The move from pilot to full commercial adoption requires robust regulatory frameworks that treat digital assets and stablecoins as equivalent or superior substitutes for legacy payment instruments, while mitigating risks associated with regulatory arbitrage and illicit finance.

Market Impact: Banks and financial institutions are rapidly moving from passive observation to active integration. This race is not just about adopting a new technology; it is about capturing the first-mover advantage in redefining the rails of international trade and remittances, making financial services faster and cheaper for everyone.

Google Search Preference

Add Fintech Monster to your preferred sources

Never miss deep, analytical fintech insights. Prioritize our stories in your Google Search, Discover feed, and AI Overviews with one click.

About the Author

Fintech Monster

Fintech Monster is run by a solo editor with over 20 years of experience in the IT industry. A long-time tech blogger and active trader, the editor brings a combination of deep technical expertise and extended trading experience to analyze the latest fintech startups, market moves, and crypto trends.