US Banks Predict 'Slow, Then Fast' Shift to Tokenized Digital Assets in TradFi

Key Takeaways

Traditional finance is undergoing a phased structural evolution, where established banks predict digital assets and tokenization will augment—not replace—their core services, driven by regulatory clarity and institutional integration.

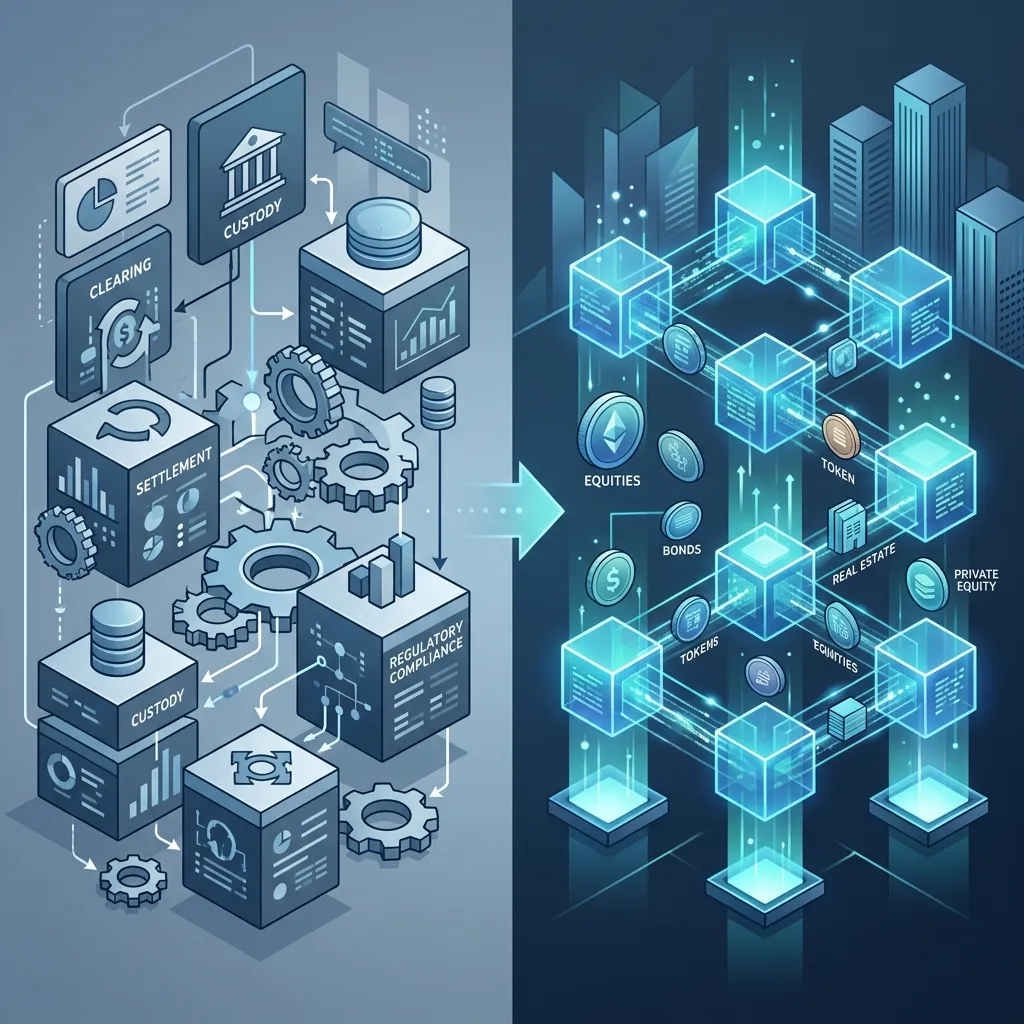

The global financial plumbing is preparing for its most profound overhaul since the rise of electronic payments. Major credit rating agencies and industry analysts predict that the integration of digital assets and tokenization into established banking infrastructure will unfold in a methodical, two-stage process: a slow, deliberate crawl toward adoption, followed by an exponential, fast acceleration across key settlement rails. This paradigm shift fundamentally challenges assumptions about counterparty risk, liquidity management, and the traditional latency inherent in large-scale financial settlements, marking a definitive move toward a hybrid system where Decentralized Finance (DeFi) principles meet the stability and regulatory rigor of Traditional Finance (TradFi).

For decades, complex financial instruments—from derivatives to fixed-income securities—have been managed by siloed, proprietary systems that involve multiple custodians and lengthy settlement windows (T+2, T+3). The inefficiency of this structure represents billions in friction costs and significant systemic risk. The core mechanism poised to resolve this friction is the tokenization of real-world assets (RWAs). By digitally representing ownership rights and claims on physical or financial assets (like US Treasuries or commercial real estate) as tokens on a regulated blockchain, the entire process of ownership transfer and collateralization becomes instantaneous and verifiable. This process does not signify the death of the bank, but rather the mandatory digitalization of the bank’s foundational ledger—making the regulated, tokenized asset the standard unit of exchange and collateral throughout the system.

How Will Tokenization Actually Reshape Global Banking?

The shift is not a singular, clean break; it is an integration layer applied over existing, robust institutions. Industry analysis suggests that the immediate impact will be focused on high-value, high-volume institutional settlements. The early phase of adoption will involve piloting the tokenization of assets that are already digitized or easily securitized, such as major sovereign debt. This allows large, cautious institutions to test the technology and quantify the reduction in counterparty risk without disrupting their core operations.

The most immediate and disruptive impact will be seen in cross-border payments and capital markets settlement. Currently, moving massive sums between jurisdictions involves layers of correspondent banking and fragmented systems, leading to settlement risk and substantial delays. Tokenized deposits and regulated stablecoins, backed by audited reserves, offer a programmable, atomic settlement layer. Instead of a multi-day, multi-jurisdictional process, settlement becomes near-instantaneous and final, thereby drastically cutting the required working capital and liquidity reserves across the board. This increased efficiency is the primary economic incentive driving the institutional adoption curve.

Why is Regulatory Clarity the Essential Prerequisite for Adoption?

Perhaps the single greatest factor governing the pace of this transition is regulatory compliance. The sheer complexity and potential systemic risk associated with transacting with unbacked or unregulated digital assets necessitate a formalized regulatory framework. The consensus suggests that the passage of clear federal legislation, similar to frameworks governing stablecoin issuance and digital reserve custody, will act as the critical inflection point.

Without explicit regulatory guidance—establishing a clear definition of what constitutes a regulated digital currency, how stablecoins must be backed, and who is responsible for the custody of digital assets—the market remains fragmented and bifurcated. The market needs assurance that the "on-chain" value corresponds directly to a legally enforceable claim in the "off-chain" world. This confidence level, achievable only through coordinated global and national regulatory action, is what will accelerate the transition from the "slow" pilot phase to the "fast" mass adoption cycle.

Key Facts

- The Catalyst: The transition is driven by the need to improve capital efficiency and reduce counterparty risk across global payment rails.

- The Role of Tokenization: Tokenization allows traditionally illiquid assets (real estate, commodities, private equity) to be fractionalized and traded digitally, vastly expanding asset liquidity.

- The Timeline: The "Slow Climb" phase focuses on niche, high-value institutional use cases, while the "Exponential Growth" phase will see mainstream retail and commercial adoption.

How Will Banks and Financial Institutions Adapt?

Financial institutions are not preparing to be replaced; they are preparing to become the custodians of the new digital infrastructure. Their role shifts from merely managing physical assets and physical settlement to providing the trust layer, underwriting, and technological rails necessary for secure digital asset management. The core value proposition remains trust, but the delivery mechanism becomes technology.

The coming decade will see a fundamental recalibration of finance, moving from physical rails and paper promises to digital rails and cryptographic assurances. The ultimate winners will be the institutions and technologies capable of bridging the gap between traditional finance's immense reservoir of assets and the limitless scalability and efficiency of decentralized digital ledger technology. This evolution is less a revolution and more a sophisticated, institutionally guided upgrade.

About the Author

Fintech Monster

Fintech Monster is run by a solo editor with over 20 years of experience in the IT industry. A long-time tech blogger and active trader, the editor brings a combination of deep technical expertise and extended trading experience to analyze the latest fintech startups, market moves, and crypto trends.