Beyond Speculation: How KuCoin's KuCard Bridges Crypto to Mainstream Commerce in Australia

Key Takeaways

KuCoin's KuCard launch signals a major maturation point for the crypto industry, providing a regulated, real-time mechanism for spending digital assets at traditional points of sale via Mastercard.

The launch of the KuCard in Australia by KuCoin represents far more than a simple debit card product rollout; it is a sophisticated strategic declaration that the cryptocurrency asset class is transitioning from speculative digital commodity to established, tangible medium of exchange. By coupling its digital asset holdings directly to the trusted global infrastructure of Mastercard, KuCoin is effectively engineering a "bridge," solving the primary historical friction point plaguing digital currency adoption: real-world, point-of-sale utility. This move positions the exchange squarely at the nexus of decentralized finance (DeFi) and traditional banking rails, promising to accelerate mainstream consumer acceptance of crypto in a highly regulated market like Australia.

Historically, the challenge for crypto payments centered on settlement risk, volatility, and lack of acceptance. Merchants, accustomed to the instant finality and predictable currency of fiat payments, have struggled to integrate volatile digital assets into their daily operations. The KuCard-AU directly addresses these systemic issues. It achieves utility by providing eligible Australian residents with a method to spend volatile assets like Bitcoin or Ethereum while ensuring that merchants receive immediate, real-time settlement in local Australian Dollars (AUD), minimizing exposure to market fluctuations and drastically reducing operational risk. This technical finesse, backed by stringent compliance, is the core value proposition transforming crypto from an investment ledger entry into a true consumer spending tool.

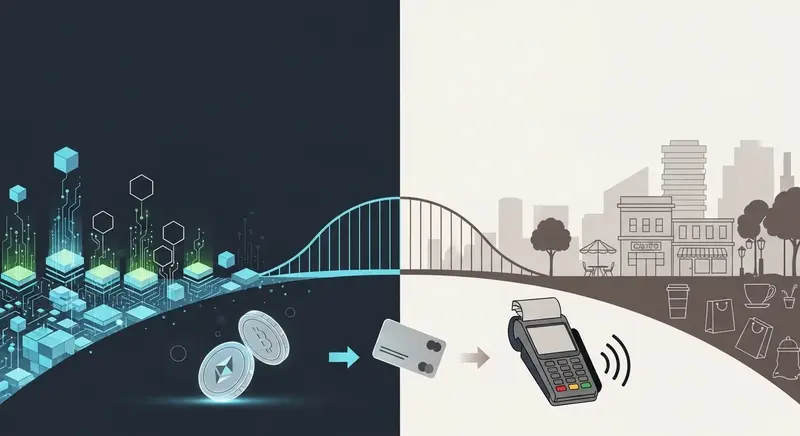

How Does KuCoin’s Card Solve the Crypto Settlement Puzzle?

The true innovation of the KuCard lies in its operational mechanics, which dismantle the inherent difficulties of cross-asset, cross-jurisdictional payments. Unlike previous experimental payment models that may have relied on delayed settlement or complex token bridging, the KuCard utilizes a streamlined, highly engineered process centered on stablecoins.

Understanding the Crypto-to-Fiat Conversion Flow

The process begins when a cardholder initiates a transaction at a merchant—be it an online retailer or a local supermarket. The system is designed to execute a multi-step, real-time conversion:

- Asset Submission: The user allocates crypto assets (such as ETH, BTC, or other supported tokens).

- Standardization via USDC: The system first processes the value of the submitted crypto assets into USDC (US Dollar Coin). USDC serves as the essential, stable intermediary settlement currency. Crucially, the initial support for 37 different USDC trading pairs ensures flexibility and depth across major digital assets, accommodating a wide range of user holdings.

- Real-Time Fiat Conversion: This is the most critical technical step. Instead of simply accepting the volatile crypto value, the system executes a real-time conversion of the USDC value into Australian Dollars (AUD) at the point of settlement. This ensures the merchant receives the exact fiat amount required instantly, removing the element of settlement uncertainty that plagued early digital currency adoption.

This real-time, USDC-mediated settlement structure provides the predictability and reliability demanded by traditional financial institutions and major global payment networks.

Why Is Mastercard Integration the Game Changer?

The technical complexity of the crypto conversion is elevated by its integration into the Mastercard network. This integration is not merely a branding exercise; it is the necessary permission layer that guarantees global acceptance.

Mastercard provides the trust, the infrastructure, and the existing merchant acceptance footprint that no standalone crypto exchange could achieve alone. By anchoring the crypto spending power through this massive payment rail, KuCoin makes the transaction virtually "invisible" to the end merchant. They simply see a successful Mastercard transaction in AUD, oblivious to the initial complex digital asset conversion that occurred minutes earlier. This seamlessness is paramount, allowing for rapid, frictionless consumer adoption across diverse sectors, from fuel stations to high-end electronics retailers.

Key Facts

- Settlement Currency: Transactions are settled in Australian Dollars (AUD) in real-time, mitigating volatility risk for merchants.

- Intermediary Role: The process utilizes stable assets (like USDC) to manage the conversion, ensuring stability and compliance.

- Market Scope: Integration with established payment rails vastly expands the acceptable merchant network beyond purely crypto-native outlets.

- Regulatory Compliance: The emphasis on regulated payment rails helps build trust and navigate evolving international financial regulations.

Navigating the Regulatory Landscape

The ability to operate smoothly within established financial rails is as important as the technology itself. The regulatory focus on predictable settlement and traceable flows allows Kucoin to establish credibility. By adhering to recognized frameworks, the platform significantly reduces the barriers to entry for merchants and consumers alike, signaling a maturation of the crypto payments space. This disciplined approach contrasts sharply with the earlier, more volatile phase of crypto adoption, grounding the technology in traditional finance principles.

Conclusion: A Maturation Signal

Kucoin’s KuCard, leveraging the backbone of Mastercard, represents a critical maturation point for the digital asset economy. It signifies the transition of digital currencies from niche, speculative assets into recognized, utility-driven payment mechanisms. For consumers, it means a reliable, convenient way to spend crypto assets; for merchants, it means access to a growing, digitally native customer base without the operational headache of handling volatile digital assets directly. This infrastructural achievement solidifies the narrative that crypto is not just an asset class, but a genuine, functional payment infrastructure, poised to reshape global commerce.

Google Search Preference

Add Fintech Monster to your preferred sources

Never miss deep, analytical fintech insights. Prioritize our stories in your Google Search, Discover feed, and AI Overviews with one click.

About the Author

Fintech Monster

Fintech Monster is run by a solo editor with over 20 years of experience in the IT industry. A long-time tech blogger and active trader, the editor brings a combination of deep technical expertise and extended trading experience to analyze the latest fintech startups, market moves, and crypto trends.